Accounting Treatment of Letters of Credit (LC) for Domestic Purchases in India

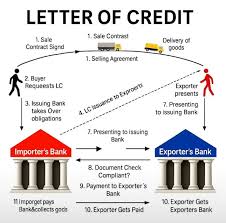

Letters of Credit (LCs) are widely used by Indian businesses to provide comfort to suppliers that their payments will be honoured on time, especially where the ticket size is large or the credit period is long. An LC is essentially a bank’s undertaking to pay the seller, subject to fulfilment of specified conditions, typically linked to supply of goods or services and submission of agreed documents. For domestic purchases within India, LCs are increasingly common in sectors such as steel, chemicals, bulk pharma, engineering goods and large project supplies.

Wiki : https://en.wikipedia.org/wiki/Letter_of_credit

From an accounting perspective, many finance teams are unsure whether the LC itself should be recognised as a liability, or whether the usual trade creditor treatment is sufficient. The confusion is greater in the case of usance LCs, where payment is made after a deferred period such as 30, 60 or 90 days. In practice, the LC is usually a payment mechanism and a risk‑mitigation tool, while the underlying liability continues to be the normal trade payable to the supplier. The key is to align your entries with the substance of the transaction while also meeting disclosure requirements on contingent liabilities and commitments.

Business scenario: Domestic LC for deferred payment

Consider a common scenario: a company purchases goods worth Rs 1 crore from a domestic Indian vendor, on terms that payment will be made 90 days after receipt of goods against a usance LC. The vendor wants comfort that the payment will be made on due date and therefore insists on an LC from the buyer’s bank. The buyer’s bank issues the LC in favour of the vendor, assuring payment on presentation of compliant documents after the 90‑day period. For the buyer, this arrangement is similar to obtaining short‑term supplier finance from the banking system, supported by the LC limit sanctioned by its bank.

From the buyer’s accounting point of view, there are three distinct elements in this transaction: recognition of purchase and inventory, recognition and clearance of trade payables to the vendor, and accounting for bank‑related items such as LC commission, margin money and any interest or charges on the deferred payment. If the accounting policy is not documented and communicated clearly, you may see inconsistent practices across branches or units, leading to reconciliation issues and avoidable audit qualifications. A clear policy backed by robust ERP configuration removes these pain points and improves reliability of financial reporting.

Option 1: LC as a payment mechanism, vendor as the main liability

Under this approach, the company records the purchase and trade payable in the usual manner when the goods are received or the vendor invoice is approved. The LC is treated purely as a payment mechanism and a bank commitment; it does not replace the vendor liability in the books. The vendor continues to appear as a creditor until the bank actually makes payment under the LC and the buyer’s bank account (or LC settlement account) is debited. Only bank charges, LC commission and any margin money are separately accounted for as expenses or assets, as the case may be.

This approach is conceptually clean and consistent with the principle that liabilities arise from obligations to suppliers, not from the existence of an LC facility. It also aligns well with the framework on provisions and contingent liabilities, which requires that contingent items generally be disclosed in the notes rather than recognised as separate liabilities. Since the vendor account remains active until payment, creditor ageing reports, vendor reconciliations and trade payables disclosures remain straightforward and transparent. For most domestic LC‑backed purchases, this is a robust and widely accepted method.

Option 2: Using an LC control account for internal tracking

Option 2: Using an LC control account for internal tracking

Some entities prefer to introduce an LC control account in the general ledger to monitor limits and utilisation more closely. In this method, the underlying accounting recognition stays the same (purchase and trade payable on goods receipt), but an internal account such as “LC Control Account” or “LC Payable – Bank XYZ” is used for tracking. For example, at the time an LC is opened, the finance team may pass a transfer entry between the vendor and LC control ledgers for internal MIS, and reverse or adjust it at the time of settlement. The objective is not to change the nature of the liability, but to improve visibility of the LC‑backed payables.

The benefit of this approach is that treasury and finance teams can generate more granular reports: how much of the LC limit is utilised, what is the maturity profile of LCs, and which vendors are backed by which banks. This is particularly useful in large groups managing multiple LC facilities across several banks. However, if not carefully designed, there is a risk that the LC control entries may be misunderstood as creating or extinguishing liabilities, leading to duplication or understatement of trade payables. Clear documentation of journal logic and periodic reconciliation between vendor ledgers and LC control accounts are essential safeguards.

Option 3: LC disclosed as contingent liability or commitment

A third angle to consider is not so much about the journal entries, but about disclosure in the financial statements. Since an LC represents a bank’s contingent obligation to pay, backed by the buyer’s promise to reimburse the bank, it is often disclosed as a contingent liability or commitment in the notes to accounts until it is drawn or settled. Under the Indian accounting framework aligned with Ind AS 37 and similar guidance, contingent liabilities are generally not recognised on the face of the balance sheet but may be disclosed to provide users with information about possible obligations and commitments.

For a domestic LC where the underlying purchase and trade payable have already been recognised, the LC may be shown as part of the company’s banking facilities, guarantees and commitments. This improves transparency for lenders, investors and other stakeholders, giving them a better picture of off‑balance sheet exposures and banking arrangements. The flip side is that if these disclosures and internal registers are not maintained carefully, management may underestimate the cumulative impact of LCs on liquidity planning, interest costs and bank covenant compliance. A disciplined note‑disclosure process, supported by a regularly updated LC register, addresses this concern effectively.

Choosing the right approach for your organisation

For most Indian businesses using LCs to support domestic purchases with a fixed credit period, treating the LC as a payment mechanism (Option 1) while maintaining a separate LC register and appropriate disclosures (Option 3) offers a good balance between simplicity and transparency. Larger or more complex organisations may additionally adopt an LC control account structure (Option 2) to achieve better internal monitoring of limits, maturities and bank‑wise exposure. The right choice depends on your scale, complexity of banking arrangements, ERP capabilities and reporting requirements from lenders or investors.

At MLG Associates, we help clients design and implement practical accounting policies for trade finance instruments such as letters of credit, bank guarantees and buyer’s credit. This typically includes mapping the entire LC life cycle in the ERP, defining standard journal entries for each stage, documenting policies on classification and disclosure, and training internal teams so that the process runs smoothly across locations. With the right structure, LCs can become a powerful tool to manage working capital and supplier relationships, without creating confusion or inconsistency in your books of account.

Suggested reference links for the bottom of your page:

-

ClearTax – “Letters of Credit – Definition, Types and Process” – https://cleartax.in/s/letters-of-creditcleartax

-

Buyers Credit Accounting Entries – https://buyerscredit.in/2011/10/19/accounting-finance/buyerscredit

-

GKToday – “Usance Letter of Credit” – https://www.gktoday.in/usance-letter-of-credit/gktoday

-

Ind AS 37 summary – MYND Glossary – https://www.myndsolution.com/glossary/ind-as-37/myndsolution

-

IFRS – IAS 37 Provisions, Contingent Liabilities and Contingent Assets – https://www.ifrs.org/issued-standards/list-of-standards/ias-37-provisions-contingent-liabilities-and-contingent-assets/ifrs